Gold Rush from London? Not True, Not New

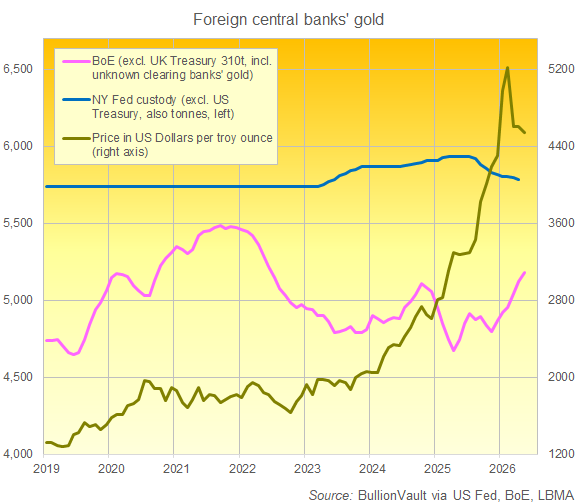

Bank of England gold custody hits 4-year high...

WHERE should central banks keep their gold? asks Adrian Ash at BullionVault.

It's a question which, over the past couple of decades, we've touched on once or twice if not a dozen times.

But it's not our question today. Not yet.

No, our starting question today isn't where should central banks keep their gold, but where do they keep it right now?

Cue the Financial Times:

"Global central banks are removing gold from vaults in London and New York," says the FT, launching a thousand copy-n-paste pieces, "as they become more skittish about storing bullion outside their borders."

Nations are pulling gold out of London, you say? And out of New York too?

Well, no. Not quite.

Any clickbait you've seen has over-read the story, ignored the actual data, and hyped up the hype.

But while the story isn't true today, it isn't exactly wrong. Nor is it new either.

I mean, we noted this decade's great central bank gold buying skipping London storage back in 2022. When outflows were actually happening.

The current spate of headlines start with the latest survey of central bank reserves managers conducted by the mining industry's World Gold Council.

This is the 9th such survey from the WGC, and excellent insights it offers, too.

This year's survey finds that, with prices tripling from a decade ago, central banks think gold is a great asset to hold. Albeit not quite as great as they thought last year.

Maybe that's because gold prices rose 20% during the Feb-to-May window of the 2025 survey, but lost 12% from February's record to late-May this year when the 2026 poll was taken.

Still, "Respondents overwhelmingly (89%) believe that global central bank gold reserves will increase over the next 12 months" (down from 95% in 2025).

"A record 45% of respondents expect their own gold reserves will also increase over the same period" (up from 43% in 2025).

"The majority of the remaining respondents indicated they expect no change [to the size of their own gold reserves] while 1% expect their institution’s gold reserves to decrease" (no one said they expected to cut gold in 2025).

Little change, in short. Central banks love gold. And where do today's gold-loving central banks choose to keep their metal?

Per CNBC's summary:

"A total of 9% of respondents said they increased domestic storage over the past 12 months, up from 5% a year earlier. Another 10% said they diversified their overseas storage locations, compared with just 2% in last year's survey."

Add those 2 together, and the figure of nearly 1-in-5 central banks who say that since spring last year they either added gold at home or rearranged where they hold it abroad is well over twice the figure in any of the prior 5 surveys...

...signalling deeper concerns, perhaps, over the security of where and who looks after their metal.

In fact, that proportion is right up there with the survey of − oh! − eight years ago in 2018, when a huge 17% of respondent's told the WGC's first such survey that they had increased their domestic storage of gold over the prior 12 months. (It didn't ask whether anyone had shuffled their foreign-held holdings.)

So yes, the appeal of holding some gold at home is definitely a thing. But it remains very far from a rush. And it's also very far from new.

Look back 15 years for instance, and time was that the Bank of England...

...historically and practically-speaking THE centre of the global gold market, and still the primary site for central banks to hold at least some of their gold today if they want to trade or lend it out...

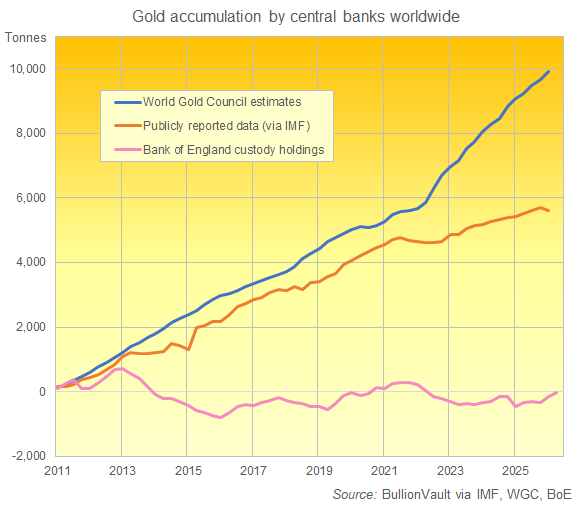

...saw the tonnage in its custody rise in line with the total tonnage owned by central banks as a group, as reported by their public data.

Back then, in 2011, the quantity of gold kept at the BoE in London also rose in line with analyst estimates of the 'true' accumulation, such as the figures reckoned and published by the WGC in its excellent Gold Demand Trends reports.

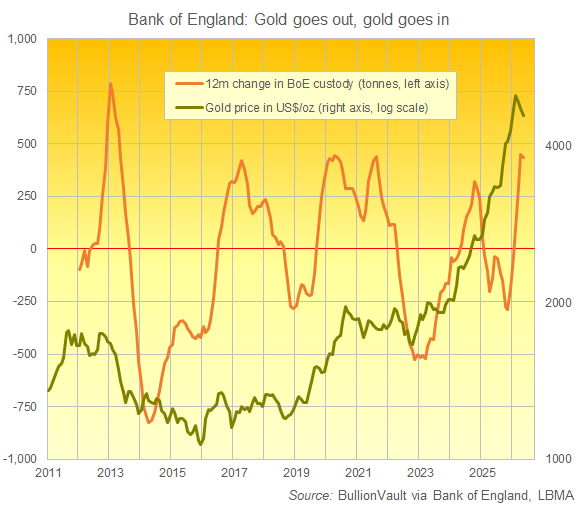

But London's appeal clearly began to break down starting in 2013, when the BoE's custody holdings actually shrank as global central bank holdings continued to rise. That was a year before Russia stole Crimea, it was nearly a decade before Russia invaded Ukraine in 2022, prompting the Western financial sanctions which everyone keeps saying have driven central banks to buy lots of gold and keep it all at home.

As for the New York Fed, the actual data agree with the WGC survey that foreign-owned metal has recently left the care of the world's largest single custodian. But as of May 2026, it had only shrunk by 2.5% from what was an 11-year high in spring 2025...

...dropping by 202 tonnes on our maths, most of it no doubt accounted for by the Banque de France selling the final 129 tonnes of its US-held gold to re-buy the same quantity and hold it in Paris, keeping its total gold reserves at 2,436 tonnes.

London has meanwhile seen the quantity of gold entrusted to the Bank of England by other central banks rise to a 4-year high. And across the London market more broadly, the same story: a 4-year high for total custody holdings by weight. Strip out the BoE figures, and that puts commercial bank and specialist logistics warehousing for private investors and traders...

...including the 8.0 tonnes securely stored and insured for BullionVault clients at Loomis in London...

...down very slightly in May (-2.0%) from March's peak.

Such a drop in London's total private gold custody is only to be expected as prices retreat from the New Year spike, helping revive end-consumer demand elsewhere as shareholders in gold ETFs liquidate stock, forcing a new outflow from those trust funds, most of which are backed by London-held metal.

But the "withdrawal" of central bank gold from London? It's simply not true today. Nor is it news.

If you wanted to panic or gasp about gold leaving London, then 2025 offered a much better time.

But nothing as good as the 2022 gold outflows from London or, best of all on the available data, 2013-2014.

This ebb and flow simply isn't news, in short. Indeed, it's exactly how the majority of central banks answering the WGC's survey say that they go about acquiring bullion...

...buying it (or trading derivatives) on the "global market" (ie, London)...

...if not arranging "off market" deals with other central banks (ie, almost certainly through London)...

...and then either leaving it there (ie, London) or flying it elsewhere according to maybe 62% of respondents (depending on how you count the replies to Question 20).

That doesn't mean "repatriation" isn't a thing however. It simply isn't a new thing.

Nor does that mean domestic gold storage isn't a really big trend among central banks. Make no mistake about that.

But to get back to the headlines, where does this idea that central banks are pulling gold out of London and New York come from?

Well, question 26 in the WGC's survey asked "Where do you currently vault your gold reserves? (Select all that apply)."

By far the most dramatic winner this year was "Prefer not to answer"...

...a box ticked by 20% of this year's respondents against 8% of last year's replies, and an answer which suggests that 1-in-8 central banks have suddenly become coy about where they choose to hold their gold.

Thing is, it's not this year but that reading from 2025 which is the real outlier. Because 8% really contrasts with both 2026 and with a range over the 4 years from 2021 to 2024 of between 21% and 29% for "prefer not to say".

Same thing applies to this year's London and New York "outflows".

Last year the Bank of England was named as a storage location by 64% of the WGC's central bank respondents. That dropped to 57% in 2026.

Yet this year's figure was still higher than 2022, 2023 or 2024. And it's very much in line with the prior 5-year average. Even including the outlier of 2025, that came in at 58%.

Same with the New York Fed. It has seen a drop in favour to 14% for 2026, down from 17% of the WGC's respondents last year. But that came after readings (in reverse order) of 12%, 10%, 11% and 15%.

Same for the Swiss National Bank too. It was named as a gold storage location by 12% of respondents in 2025, twice the percentage who named the SNB this year. Yet it hadn't been above 7% in the four years from 2021 to 2024. So again, the drop in 2026 is a return to pre-2025 levels, rather than being the outlier on the available data.

Still, as our analysis above shows, the move to pull gold out of New York and London is relatively true, even if it doesn't really apply today. And the Financial Times is far from alone in announcing what changes there are like it's breaking news.

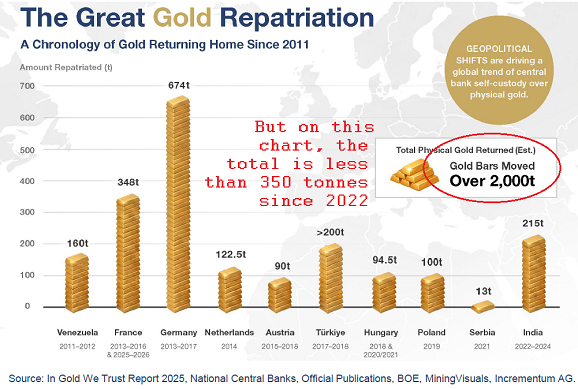

'The Great Gold Repatriation' is what the latest must-read report from Swiss advisors and fund managers Incrementum calls it.

"Geopolitical shifts are driving a global trend of central bank self-custody over physical gold."

Long-term, that's true. But here again, even amid the insights and always provocative analysis of Incrementum's In Gold We Trust report, the examples shown are far from new...

...with 8 of the 10 central banks listed by the latest IGWT actually shifting gold home before the Covid pandemic of 2020, never mind the anti-Russia sanctions spurred by Putin's 2022 invasion of Ukraine.

Six of those 8 moved gold home a decade ago or more...

...and the other two (Serbia and India) have done the same as Poland did in 2019 (to much fanfare), which was to buy gold in London and then fly it home.

That makes "repatriation" a bit of a stretch. Going "shopping" is closer maybe.

That said, and as our top 2 charts above show, the huge accumulation of central bank gold in more recent years has clearly skipped London or New York storage. But the news about central banks pulling gold out isn't true right now, even though it isn't false either. And it most certainly isn't new.

As for where central banks should hold their gold, well...that would be a political matter.

And the politics aren't good. Even if they aren't causing anything like a flight of gold out of the West's major gold custody and trading centres today.

Email us

Email us