Which Country Owns the Most Gold? Gold Reserves By Nation

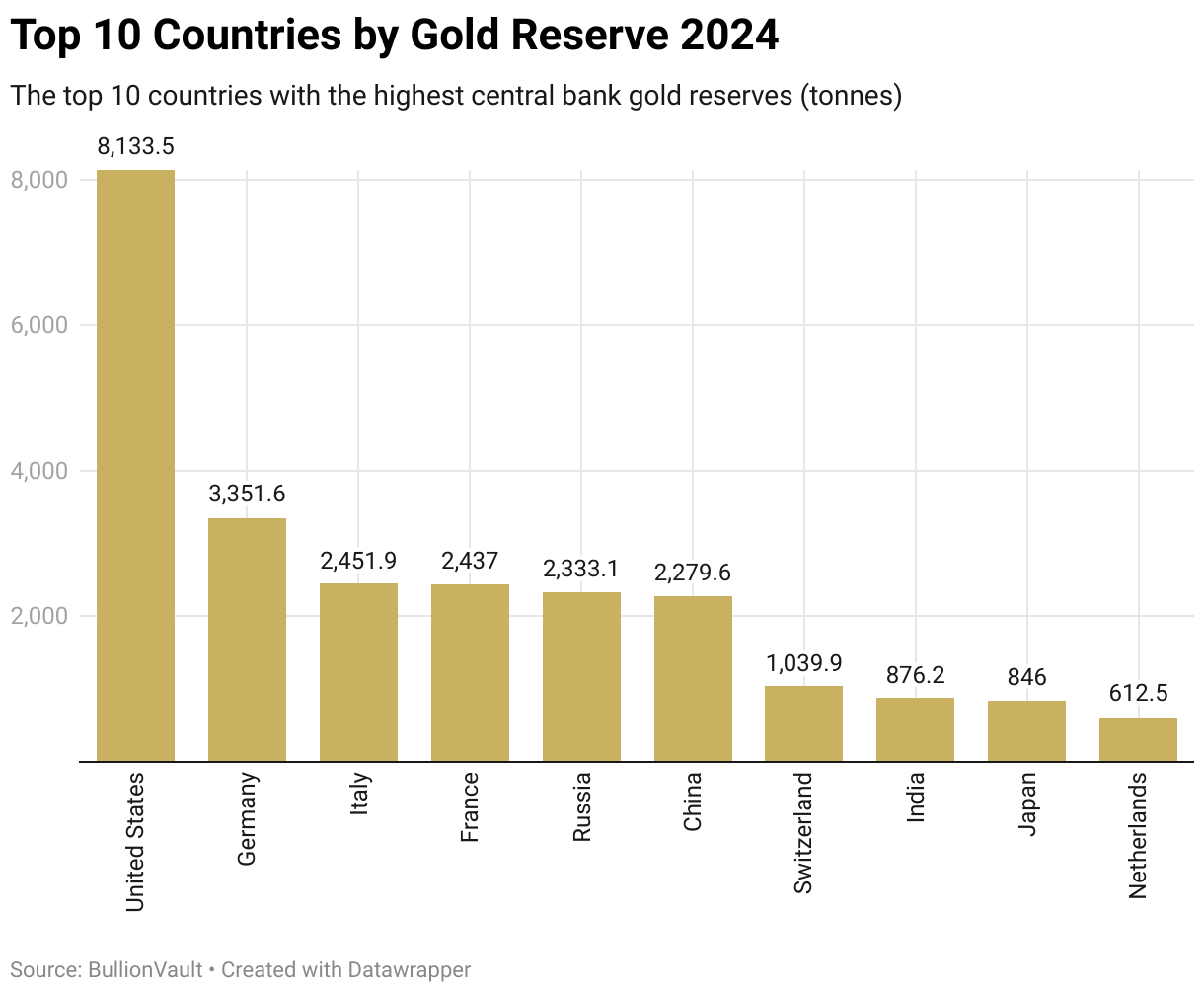

Top 10 countries by gold reserves 2025

USA

Germany

Italy

France

Russia

China

Switzerland

India

Japan

Netherlands

Who is buying the most gold among central banks and why?

China

India

Poland

Countries doubling their gold reserves

Russia

Why do central banks buy and hold so much gold?

How much gold does the UK have?

Why are UK gold reserves low?

Uses of gold FAQs

Gold has been used in jewelry for thousands of years primarily due to its appearance and natural lustre that doesn’t diminish over time due to gold’s inertness and resistance to tarnishing. Pure gold is relatively soft and easy to craft into delicate and intricate pieces and can also be combined or alloyed with different metals to change its colour and hardness.

The global wholesale gold investment market, centred in London deals in the London Good Delivery gold bullion bar. This London Good Delivery bar weighs 400 troy ounces - about 12.4 kilograms - and is about eleven inches long. It is stamped on the top (the larger face) with the manufacturer's name, the weight, and the assayed purity. The minimum specified fineness must be 99.5% pure gold, but improvements in the refining process mean that Good Delivery bars now reach 99.99% purity or higher.

In the UK gold jewelry is subject to Value Added Tax (VAT) at the standard rate of 20%. In the UK gold jewelry is considered a consumer good much like a mobile phone or TV. However, investment grade gold bullion in the form of London Good delivery bars or investment grade coins and small bars can be bought and sold free of VAT.

Since 2010 the percentage of gold used for investing has averaged 29%. 2013 saw the lowest investment percentage at 18% and in 2020 during the Covid pandemic the percentage of investment gold peaked at 49%. If you include Central Banks reserves as gold investment of sorts, then between 2022 and 2024 this reached 23% of gold demand.

Between 2010 and 2024 the percentage of gold used in technology has averaged 8% with little variation over the past decade. In comparison over the past 15 years gold used in jewelry has accounted for 50% of total gold demand.

Central Bank Gold Reserves