Gold and Silver Sink as Death of US-Iran MOU Sends Oil, Rates Jumping

GOLD and SILVER PRICES sank on Wednesday after US President Trump said the peace deal with Iran is "over", sending crude oil and interest-rate expectations sharply higher amid continued attacks on shipping through the Strait of Hormuz.

Hong Kong meantime marked the 2nd day of its new gold clearing and settlement system, with a raft of banks, wholesalers and data providers issuing press releases to claim their place "among" the first participants and supporters.

"I don't want to deal with them anymore, they're scum," President Trump said this morning of the Tehran regime at today's Nato summit in Ankara, Turkey, while also telling his Secretary of State Scott Bessent to "cut off" all trade with Nato ally Spain for failing to spend enough money on defense.

Silver prices lost over $2 per troy ounce within 45 minutes of Trump's remarks, dropping near to $58, while gold lost $80 per troy ounce within 2 hours to $4041 before also steadying as crude oil edged back from its steepest jump in 2 months.

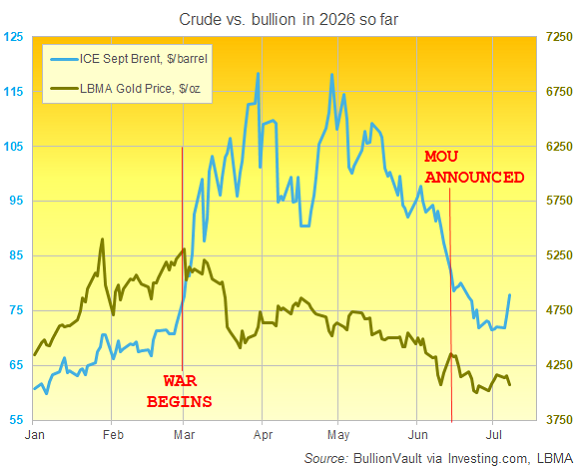

Having fallen to the lowest price since the eve of the US and Israel starting all-out war with Iran on the last day of February, crude oil today leapt as much as 6.7% to touch the highest since mid-June − when the MOU was first announced − back above $74 per barrel of Brent for September delivery.

Interest rates on US Treasury debt also extended the rebound already building this week, peaking above 4.58% per annum on 10-year bonds, the highest in almost 6 weeks.

Looking back to gold and silver's record all-time highs, set ahead of the Iran war, "Most of the weak-handed and or speculative holders have almost certainly been washed out over the past 6 months," says analyst Rhona O'Connell at brokerage StoneX, "and this gives gold some upside headroom.

"[But] gold is looking at the [wider] markets through the prism of the interest-rate outlook...[with] incoming Fed Chair Kevin Warsh delivering a more hawkish tone than expected" after being nominated by famously low-rate-loving Trump.

Today's jump in crude oil prices, driven by the fresh fighting and breakdown in US-Iran peace hopes, betting on US interest rates put the odds of a rate rise at the Federal Reserve's July meeting in 3 weeks' time back above 1-in-3, with a rise by end-September now seen as a 2-in-3 certainty.

"Even at [June's] depressed prices compared to [February's] over $5000/oz," says a trading update from US bullion dealer and coin retailer Fidelitrade, "the [trading] desk managed sell orders from customers locking in plentiful returns in gold.

"Volumes were 30% more on the sell side."

Gold-backed exchange traded trust funds worldwide meantime saw shareholders liquidate stock spurring over 74 tonnes of outflows, data from the mining industry's World Gold Council says today, the heaviest net selling by gold ETF investors since September 2022 outside of March's Iran war 84-tonne sell off.

"Most of gold's correction seems to be long liquidations as opposed to people taking on short exposure," says Canadian bank TD's Bart Melek.

"So there's a lot of room to expand" bearish betting.

Ahead of Trump's remarks on Iran, gold prices had already fallen overnight Wednesday in No.1 consumer nation China, where the Shanghai Gold Exchange ended with its lowest benchmark price in almost week in Yuan terms at ¥901 per gram and that price − relative to quotes in global trading and storage hub London − widened its discount to $5 per troy ounce.

Both the Bloomberg and LSEG financial data agencies say they have "supported" the development and launch of Hong Kong's new HAU gold price ticker as part of the 'special administrative region's new gold clearing and settlement system launched Tuesday.

Swiss bullion refining and finance group MKS Pamp, UK-listed banks Standard Chartered and HSBC, plus Chinese bank CITIC, are all cited in various media reports today as among the first companies to use the new Hong Kong market.

Email us

Email us