Gold Price Rallies to $4500 Despite ETF Selling and China Liquidity Slowdown

GOLD and SILVER PRICES rallied from 1-week lows on Thursday, recovering the $4500 and $75 marks despite news of ETF selling and weak demand in No.1 consumer nation China as Israel and Lebanon agreed a ceasefire deal and crude oil prices sank after US lawmakers backed a move to move President Trump's war with Iran.

Israel continued its airstrikes however, and Trump slammed the House of Representatives' vote, calling the four Republicans who broke ranks to back it "unpatriotic".

"China's gold buying fever has been dampened by a sharp reversal of People's Bank's liquidity injections," says analyst Michael Howell.

"The PBoC has removed a whopping RMB 1.8 trillion (US$260bn) of liquidity, or roughly 4.5%, in just 12 weeks."

But "liquidity conditions remain quite ample at this point," says Greater China economist Lynn Song at Dutch bank ING, adding that the PBoC "is likely only looking at the short-term environment rather than signalling a shift in the broader monetary policy direction" by making zero short-term liquidity loans to China's banking sector this week, the first such pause since August 2024.

China's domestic gold demand, as indicated by bullion withdrawals from the Shanghai Gold Exchange, fell in May to the lowest since the Covid lockdowns and gold-buying collapse of 2020, totalling less than 64 tonnes.

Chinese gold mining stocks fell hard on Thursday, with Zijin (SHA: 601899) down 3.0% to test its lowest share price in 6 months after North America's HUI Gold Index of gold-producer stocks sank by 3.5% on Wednesday, outpacing the 0.7% drop in New York's broad S&P500 index from Tuesday's fresh all-time high.

Outflows from gold-backed exchange-traded investment funds listed in Asia more than matched North America's net selling in May, according to data compiled and published by the mining industry's World Gold Council.

Worldwide, gold ETF investors liquidated shares worth $2.2 billion last month, shrinking the sector's bullion backing by more than 16 tonnes to reverse half of April's net demand, putting total holdings at 4,121 tonnes.

China was overtaken in 2025 as the world's No.1 gold mining nation by Russia, figures given by Moscow's Natural Resources Minister Alexander Kozlov would claim.

Compared with specialist-analyst estimates of 330-to-360 tonnes, Russia's gold mines produced over 480 tonnes last year, Kozlov said, speaking to the Tass news agency at the 'Russian Davos' business summit in St.Petersburg and issuing an official annual estimate for the first time since President Putin began his attempted invasion of Ukraine in 2022.

While Ukraine struck St.Petersburg with drone attacks yesterday − and Russian central bank chief Elvira Nabiullina is skipping the event − Putin "failed to intimidate foreign diplomats and drive them out of Kyiv," said Ukraine's Foreign Minister Andrii Sybiha after officials from all 32 Nato military alliance member nations visited the would-be Nato member's capital city together with the alliance's General Secretary Mark Rutte.

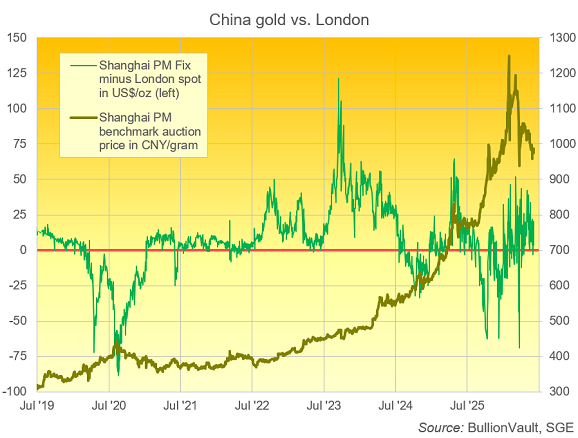

Gold prices in Shanghai today fell back to a small discount against London spot market quotes, suggesting weaker demand versus supply in China.

Trading volume on the Shanghai Gold Exchange is on track for its quietest week since end-August according to analysis by BullionVault, while the US CME derivatives exchange's Comex futures shows its lowest weekly volume since December 2024.

Email us

Email us