What Germany's Gold Shipments Mean for You

The real gold signals behind all this sturm und drang over Bundesbank holdings...

GERMANY's BUNDESBANK is rightly famed as the world's least stupid central bank, writes Adrian Ash at Bullion Vault.

Capping German inflation at single-digits all through the 1970s sure helped. Everyone else got double digits or worse (the UK and Italy got over 20% each, twice). The Bundesbank boosted its reputation further by not selling any gold at two-decade lows in the late 1990s. Not even the Swiss National Bank managed to sidestep that amateur's mistake. (Its since gone on to embrace inflation, actively creating Swiss Francs solely to devalue them.)

So where the Bundesbank still controls policy (as a Euro member, Germany has its interest rates set by the European Central Bank), it pays to pay attention. And this week's news on Bundesbank plans for gold in 2020 offer four clear lessons for anyone buying gold today.

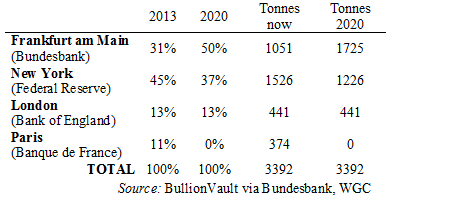

First, the facts – with BullionVault's analysis based off the Bundesbank's own news release, and the World Gold Council's compilation of the latest data on Germany's gold reserves.

What with being a fool's paradise and all, plenty of stories on the internet will tell you that Germany is "taking home its gold". But as you can see, it isn't. Fifty per cent will stay overseas. So you might want to look askance at anyone who runs such headlines.

You might then consider what the news does in truth signal...

#1. Hold gold for the long run

Based on the figures in the Bundesbank's announcement, it's clear that the German central bank has no intention of selling gold anytime soon. Its huge gold reserves, the second-largest after the United States', underpinned the Deutsche Mark's famous stability during the Great Inflation of the 1970s. Germany then refused to sell any of its gold reserves when prices were low a decade ago, unlike every other European state except Italy.

Besides very small quantities for commemorative coins, it has steadfastly refused to sell into this rising market either. Short of "the need arising", the Bundesbank has every intention of keeping hold of its gold through 2020, too.

#2. But keep it ready for sale

Despite all the fuss about "taking home its gold", Germany is keeping 50% split between London and New York. It's pulling out of Paris entirely, citing the need for foreign currency in a crisis, which France can't now offer. But the fact is that Paris doesn't offer a deep, liquid market for wholesale bullion. Whereas London, like New York and Zurich, remains a world centre for physical gold bullion. Indeed, London is the heart of global dealing, with wholesale prices worldwide always quoted as the price for London delivery plus a premium for shipping elsewhere.

The Bundesbank makes plain that, if some unspeakable crisis demanded it, being able to sell its gold fast is a prime concern. Hence the 37% staying at the New York Fed, and the 13% staying in London.

#3. And let geography spread your risk

Holding some gold overseas isn't a problem, then. Indeed, it's benefit of gold's deeply liquid international market. Because when asked, central bankers will repeatedly cite the diversifying power of gold as a major reason to own it. (See this French central banker speaking in 2000, for instance.) Unlike other metals and commodities, gold is not tied to the economic cycle, nor the stock market. It is a natural "hedge" against the US Dollar too. And if you are spreading your investment risk with gold, why not also spread your geographical risk by owning some gold overseas as well?

Historically, the reason that Germany holds gold in the UK, France and US was fear of Soviet invasion. Even with that fear gone, however, geopolitical diversification clearly still makes sense to Frankfurt – starting with a full 37% of its gold being on a separate continent. For private individuals, holding investment-grade gold in secure, professional vaults can cost you just a fraction of a per cent each year. It need cost no more overseas, and that will give you an escape fund if things get really ugly at home.

One last point – the Bundesbank has of course been very reluctant to make this move. It goes against the "gentlemen's agreement" between central bankers – the assumption that each is to be trusted, because they hold themselves and their colleagues as independent from politics and the state. But to be fair, the Bundesbank brought the demands for repatriation and especially for audits of Germany's gold all on its own head. Just in the same way as the US Federal Reserve will surely be forced to audit the US Treasury's gold at Fort Knox in due course, too.

There is no need for secrecy. Redacting sections of the most recent audit of New York-held metal (2011 was the first such visit since the early 1980s) only fuels suspicion where none should be necessary. If you hold physical gold at arm's length – whether in London or in another major centre like New York or Zurich – you'd be sure you get plain proof of your gold's quality and safe delivery inside the vault, with regular checks thereafter. You'd no doubt want to use independent professionals, whose specialism is judging the fineness and market-readiness of physical gold, to conduct the checks and then report back to you.

This is what BullionVault users do, for instance. Each year, independent assayers go into the vaults we use (Viamat AG and Brinks Inc. – both independent, London Bullion Market Association-accredited custodians) to check the sound, secure presence of all the gold and silver recorded on the Bar Lists which the custodians send. More importantly, each day we publish those Bar Lists, for all BullionVault users to scrutinize, together with the full list of all client holdings (anonymized, of course). This way, each individual can check both that their holding is where it should be, and that the sum total of all client holdings matches with the custodians' Bar Lists – right down to the last gram – in the public reconciliation on Bullion Vault's daily audit.

Similar rigor doesn't seem too much to ask of the world's second-largest gold-owning nation. Transparency in physical gold is all to the good, both for central banks and for investors wanting long-term, market-ready diversification.

Email us

Email us