Comex Gold Warehouse Stocks: How It Works

Wed, 24-Jul-2013 20:49

What does the 2013 plunge in Comex gold warehouse stocks really mean...?

THERE IS a lot of misinformation recently about Comex warehouse gold stocks, writes Miguel Perez-Santalla at BullionVault.

Most notably, there's confusion about how this year's sharp drop in the quantity of gold bullion in stock might point to some looming shortage of metal to settle gold futures contracts, or even signal an outright default by sellers to buyers.

But there is no mystery or hidden agenda of how Comex works. In this article our goal is to explain how the Comex works in the simplest fashion. Having been involved in the physical gold markets for thirty years – both making and taking delivery on the exchange, as well as through off-exchange deals for miners, refiners, fabricators and investors – I hope I'm in a position to share a true "insider" view, the better to inform this debate properly.

First question: How does gold get into warehouse stocks of the futures exchange? Although it's a lengthy process, the answer is actually quite simple. Gold is recovered either from mine output or scrap jewelry and other products, such as bars and coins, at a refinery. The refiner then produces gold bars to the standard and specification of the exchange, in this case the CME Group.

These gold bars belong either to the refiners themselves, meaning they have bought and own the gold. Or they belong to the refiner's customers, who bought and owned the gold at the refinery, hiring it to make that metal into saleable bars.

Now, for this particular refinery to deliver metal onto the commodities exchange, it must be a registered acceptable brand, such as Heraeus, Johnson Matthey or Metalor Technologies to name a few.

Once these gold bars are produced, the metal must then be transported to the warehouse by exchange-approved carriers such as Brinks Inc., Via Mat International or IBI Armored Inc. There is no other way for the gold to get onto the exchange. Gold may move between Comex-approved warehouses, such as those operated by HSBC Bank, Brinks Inc., and Scotia Mocatta Depository. But any moves made between these warehouses must be made using the same approved carriers. No gold can enter the marketplace from outside of this refining loop.

Once gold is removed from an exchange-approved warehouse and held somewhere outside of this circle of integrity, there is no way for the CME exchange to guarantee the bar's quality. This means that once a person or investor removes bars from the warehouse, then to return them to the exchange they would need to start at the beginning again. By going through the hands of the gold processor and refiners, this provides guarantee of the standard and quality of the material being delivered on the exchange.

So with the gold inside the warehouse, second question: When is the gold considered eligible or registered on the commodities exchange?

Answer: When acceptable bars are brought into an exchange-approved warehouse they become "eligible" for settlement of gold futures contracts traded on the exchange. So at this point, the owner of the bars may deliver them onto the exchange, and warehouse receipts are created. That is when the gold bars become "registered" stocks.

Eligible gold stocks may or may not ever become registered stocks. Why? Because the warehouse is still a warehouse and the owner may simply want to vault their metal securely, before using it to meet demand elsewhere – for manufacturing, or from investors in another marketplace, such as Asia. This eligible gold may belong to an investor, a refiner, a hedge fund, a bank or producer. Many times these people are holding the metal for their end customers. And it may move at any time, and is much more flexible than the warehouse receipts that are registered stocks.

The CME, the exchange, does not have any direct control over nor interest in the size of eligible stocks. Registered stocks however are officially recognized by the CME for good delivery on the exchange. That means that this inventory exists and is set aside to make delivery against gold futures contracts. Traders who stand for delivery, rather than cash payment, when their contract settles take delivery of the warehouse receipt. This does not change the quantity of registered stocks inside the warehouse. It remains registered, but the receipt changes ownership.

If a gold futures buyer wants to take physical delivery of the gold and "break" the receipt then this is possible. But it is a process and takes time. Once broken, if the gold remains in the exchange circle of integrity – meaning the exchange-approved warehouse – then those bars become eligible stocks. But if the gold bars are removed from the exchange-approved warehouse then they no longer are eligible and are no longer tracked in any way.

Third question then: How do the warehouse receipts work?

A warehouse receipt is a bearer instrument much like a check. It can be endorsed from one party to another. The holder of the receipt pays the storage costs. Most times when people take delivery of a warehouse receipt they leave it with their brokers. In some cases people may want to take possession of the warehouse receipt themselves. This is rare, just like with equity or bond certificates; no one actually takes delivery of the documents any longer. But it is still possible for a fee.

If a person owns a warehouse receipt, the gold that it represents is still in the registered stocks, even if they have taken physical delivery of the document. They can always redeliver these receipts onto the exchange by selling contracts.

How does the gold futures exchange work? CME Group is the largest futures exchange in the world. Many commodities, of which gold is one, are traded on this exchange. The gold exchange – which is often still referred to as the Comex, its original name prior to being bought by the CME – is the largest gold exchange by volume in the world.

On the exchange, futures contracts are traded. These contracts are agreements to deliver a specified quantity and grade of metal at a specified time. Because of the ability to margin these contracts, meaning to pay a deposit on a greater value of gold, there is a lot of liquidity in the market. Much of this liquidity is provided by speculators who are trying to make money on the direction of the gold price. This enables the gold industry – the mine producers, refiners, manufacturers and retailers – to protect themselves from market risk, hedging their exposure to price movements by trading contracts for prices in the future. This is the reason that the gold futures market exists.

Most commodity futures contract positions are closed prior to the delivery period. This means that more often than not, the people that contract to trade on the exchange liquidate their contractual commitments prior to having to take delivery. But this does not mean that all that business is founded only on speculation. For example, a jewelry manufacturing firm may contract to sell a gold contract as they physically buy gold. Perhaps because the product they are making has not been sold to a customer yet.

For simplicity's sake, imagine a jeweler needs 100 ounces of gold to make four hundred gold rings. The process may take him two weeks, and in that time period he may not want to take the price risk. So the jeweler decides to sell one gold contract (100 ounces) on the CME at the same time as he buys the physical gold for production. In this way he is hedged, which means he no longer has price risk. In two weeks' time, when the rings are ready and he has found the buyer, he sells the rings to the buyer and at the same time buys back the contract.

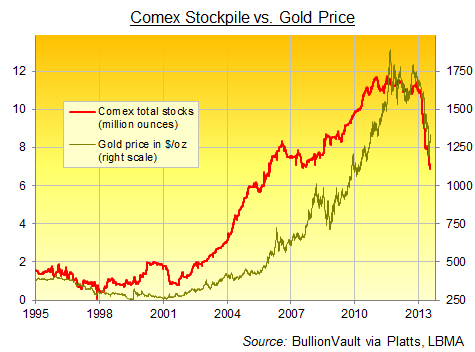

In this instance there is no settlement of physical via the commodities exchange. There are many examples similar to this one that are used every day, one way or another, for hedgers of commodities. A main factor in the gold market is that typically, when gold registered stocks are falling, that means the gold price is falling too. This indicates that gold is being better used off the market, instead of being held on the exchange. As for the total quantity of eligible and registered stocks in CME warehouses, it also tends to track prices higher and lower. When gold prices rise, it attracts more investors, who make use of gold by holding it as a store of value. This metal itself needs storing, and it's important to remember that, as we saw above, the Comex warehouses are used to do just that, alongside their role in vaulting gold bars for futures contract delivery.

The higher gold prices go, in short, the more people want to own it. So the more metal there will be held in warehouses on behalf of investors. And when prices fall, as they have in the last nine months and more, some owners of metal will find better-rewarded uses elsewhere, outside Western investment stockpiles, and converted for instance into the smaller kilobar products favored by Asian investors currently paying $20 per ounce over international prices in China.

As you can see, there's little urgency or importance in the 2013 plunge in Comex warehouse gold stocks. Gross quantities are lower, but they are greater than any period prior to 2005. Just looking at the level of warehouse stocks, it is difficult and presumptuous to extrapolate market fundamentals from the holdings of eligible or registered gold at any one time. There is still plenty of metal, and there are hundreds of millions of dollars of gold traded every day off of the Comex, for hundreds of different reasons. So this aspect of the market is only a part of a very much larger puzzle.

To get the full picture, from people in the market and experienced in studying it, look at the data and reports from the US Geological Survey, an arm of the US government that provides free information, or other firms such as the CPM Group, GFMS or Metals Focus Limited, who provide market insight for a fee.

There are lots of good reasons to buy gold today, I believe. But misunderstanding the basics of what is in truth a simple aspect of the global market shouldn’t be one of them.

Email us

Email us