Turkey's Lira Crisis Unpacked

Tue, 18-Jan-2022 09:01

Balance sheet, base money, reserves and sterilization...

TURKEY has been in the news recently due to the collapsing exchange value of the Turkish Lira,

says Nathan Lewis of New World Economics.

We have had the usual clownshow of central banks doing this, that and the other – typically, "foreign exchange intervention" and "raising interest rates", which never works.

(Nor does "lowering interest rates", which the central bank tried earlier.)

But, the situation is easy to understand, and also easy to fix, if you know how to do these things properly.

I wrote about these topics extensively in Gold: The Monetary Polaris. Also, in the past, I wrote shorter items regarding Russia, and, actually, Turkey. There is quite a lot about this topic in Gold: The Once and Future Money, a book that was inspired by the spectacle of Asian central banks making the same stupid mistakes, in the late 1990s.

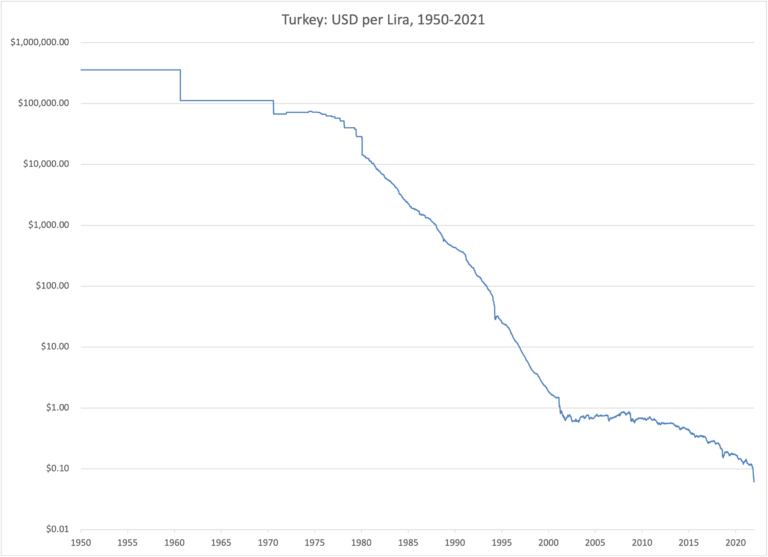

First, let's take a look at the history of the Turkish Lira.

Not very encouraging, I am sure you will agree. (Note the logarithmic scale.)

We see that the Lira was pegged to the USD, in the context of the Bretton Woods gold standard system, in the 1950s. Since the USD was also pegged to gold, at $35 per ounce in those days, the Lira was effectively also pegged to gold.

There was a rather large devaluation in 1960, and another 1970, indicating that currency discipline was already rather poor in Turkey during those days. But, Britain and France also devalued in the 1960s, so it was in the air, you could say. (The Lira appears to have a super-high value vs. the USD because six zeros were taken off in 2005. Today's Lira is worth a million old Lira.)

It's worth noting that the Lira during the Ottoman period (1844-1914) was worth 6.61 grams of gold, or about 90% of a British pound. In the past, Turkey was under the domain of the Byzantines, and the reliable gold solidus was the primary unit of account. So, there is a very long history of gold-based money in Turkey, just the same as everywhere else in the world.

During the 1970s, the Lira's value vs. the USD was somewhat stable, although there was a little variation. The Lira still appeared to be linked to the USD, but the fixed exchange rate was adjusted regularly. In this decade, emerging market countries like Turkey did not have much difficulty linking to the USD, because the USD itself was falling in value, during the inflationary 1970s. As the falling USD was brought under control by Paul Volcker in the early 1980s, ending the 1970s inflation, this proved very difficult for emerging market currencies. Many currency pegs broke in the early 1980s, followed by a regime of floating currencies – often, sinking currencies, in a decade of hyperinflation. This was common throughout the world, and looked about the same in Latin America, or some other countries in the neighborhood of Turkey, such as Yugoslavia.

However, during the 1990s, the Latin American countries got it together and stabilized their currencies vs. the USD. Turkey continued to hyperinflate during the 1990s. The rate of hyperinflation was not so great. On average, the Turkish Lira lost about 50% of its value each year, corresponding to CPI rises of about 100% per year. This is bad, but it is not the "billion-Dollar-banknote" kind of hyperinflation that you see sometimes. Also, during the 1990s, all of post-Soviet Eastern Europe (Turkey's neighbors) was also suffering hyperinflation. So, you could look at Turkey's experience as being typical of Latin America in the 1980s, and Eastern Europe in the 1990s, which makes sense.

This was not entirely because Turkey was being naughty. In both Latin America and Eastern Europe, the IMF was very involved, so the result was basically the outcome of the IMF's conventional wisdom. (Bad advice, obviously.)

In the 2000s, Turkey again had what amounted to a link with the USD, although it was a little loose, with month-to-month variation. Again, as in the 1970s, the USD was losing value (vs. gold) during this decade, so it was easier for EM central banks to link their currencies to the USD.

As the USD stabilized again in 2012-2013, this proved difficult for Turkey, just as in the early 1980s. Again, a period of declining Lira value commenced, although it was relatively slow. In recent months, the pace of Lira depreciation has accelerated – by all appearances contrary to everyone's wishes, including the government of Turkey, the central bank of Turkey, the IMF and other international bodies, and most Turkish businessmen and citizens. They have all seen this movie before, and they don't like it. But, actually, having had long experience with inflation and even hyperinflation, they also know how to deal with it. A lot of prices in Turkey are directly linked to Euros, or Dollars. If the exchange rate changes, the price (in Lira) changes, automatically. They are effectively using the Euro or Dollar as a "unit of account," with the Lira merely a "means of payment".

We see this also with Bitcoin, where prices are often in USD, but payments can be made with Bitcoin at the current exchange rate. Or, sometimes prices are directly linked to the CPI.

Either way, the Lira today is worth about a tenth of what it was in the 2000s.

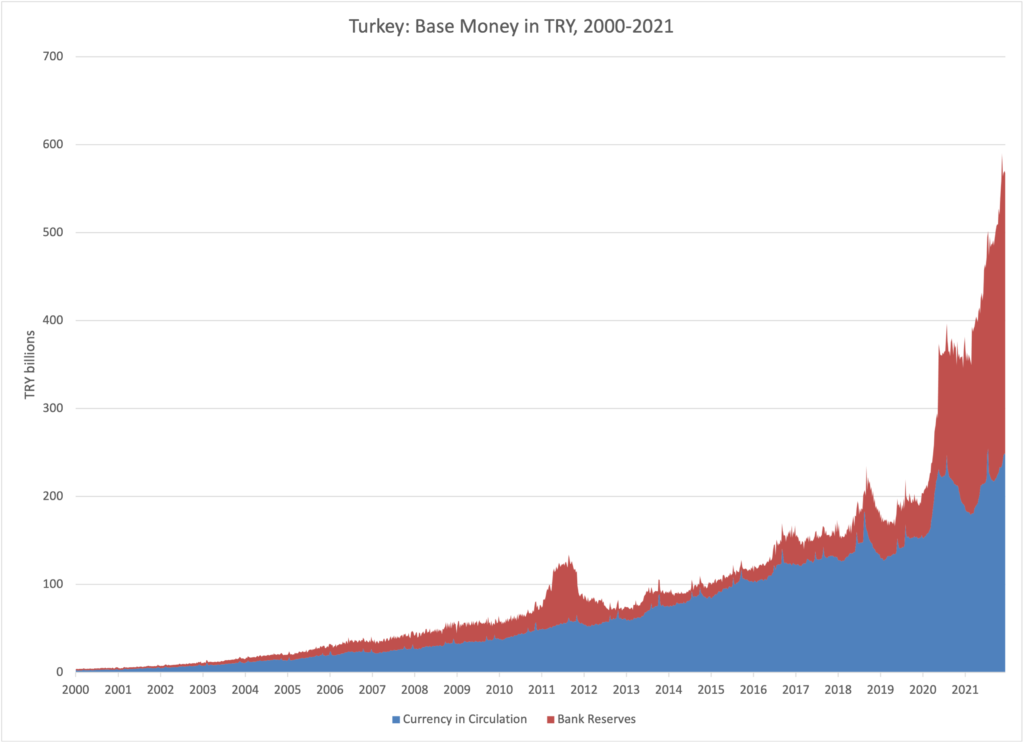

Now, let's take a look at the central bank of Turkey's balance sheet. This is easy to do, but take note – in all of the discussion that you may hear – that nobody actually does it, including the supposed "experts".

This is a measure of Base Money, consisting of two elements, currency in circulation (banknotes), and bank reserves (deposits at the central bank). I am looking at base money "ex-government" for now, omitting the government's deposits at the central bank. There are a few minor items, but these two alone capture most everything of importance.

Here we have a fairly smooth curve of growth. Bank Reserves jumped up a lot in 2020, related to Covid and also, probably, new regulatory issues such as the Basel III reforms which I have talked about in detail elsewhere.

This looks suspicious, but nearly all central banks were doing about the same thing. Then, it jumped up a lot again in 2021, which definitely looks suspicious, and is a lot harder to justify. Coming on top of the expansion in 2020, that is a huge increase in base money, especially considering the present crisis. So far, nothing has been done about it. The central bank continues to maintain high and rising base money levels. Combined with some clumsy shuffling over "lowering interest rates," it is no surprise that people started to panic.

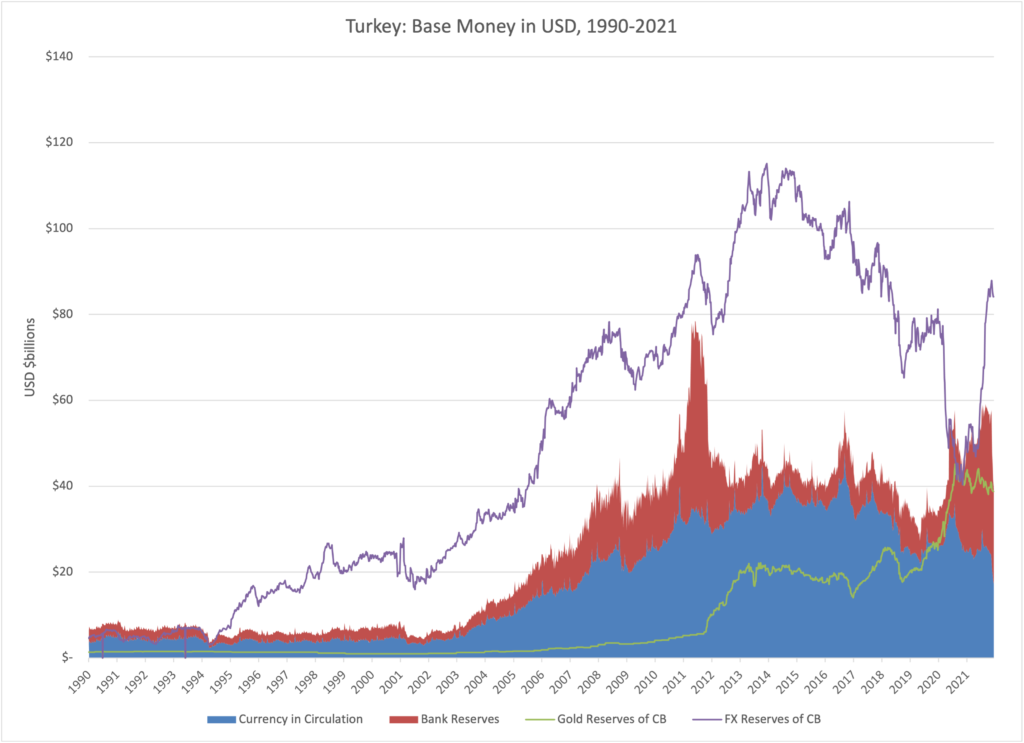

Turkey is an interesting example in many ways. But for now, cutting to the chase in terms of practical currency management, let's look at Turkey's foreign exchange reserves.

This is a chart of the value of Turkey's base money (currency in circulation and bank reserves), in terms of USD, at the prevailing exchange rates. Also, we have lines showing foreign exchange reserves, and also the value of gold held by the central bank, in terms of USD.

We see that the value of the monetary base was very low in the hyperinflationary 1990s. This is typical of hyperinflationary conditions, where nobody wants to hold much money for very long. Then, as the currency was stabilized after 2000, you could hold a lot more of it without getting beat up. So, the monetary base expanded rapidly.

Again, this is typical after a hyperinflation. This is very confusing to some people, because it involves a lot of "printing money"! Isn't that what caused the hyperinflation? But a more reliable currency has a lot more demand, and to meet that demand, there needs to be a lot more supply.

Then, as the Lira again entered a period of steady decline vs. the USD after 2011, again the Lira monetary base became rather stable in terms of USD, albeit at a higher level than in the 1990s.

Note that foreign exchange reserves (purple line) were consistently above the value of total base money. This happens because foreign exchange (Dollars) are purchased in the process of expanding the base money supply. However, as the value of the Lira declines, the central banks' liabilities (Lira) go down (in USD terms) while the value of assets (forex reserves) stays stable (in terms of USD). So, the process of "money printing" via foreign exchange acquisition leads to more and more foreign exchange. This is common among emerging market central bank balance sheets, where there has been a history of currency decline. Much the same is true of acquisitions of gold bullion as a reserve asset.

The end result of all this is that the central bank has foreign exchange reserves of about $85 billion today, plus gold worth about $39 billion. This is against base money liabilities of about $34 billion now (after a quick decline in the Lira), and about $60 billion earlier this year (before the decline in the Lira). In other words, Turkey's central bank can easily buy every Lira in existence, even at the earlier exchange rate of about 8 Lira per Dollar, which corresponds to about TRY 15,000 per ounce of gold.

So, if we were to introduce a gold standard for the Lira, at 15,000 per oz of gold (the mid-2021 rate), we would already have about 65% bullion reserve coverage. You could even take about $20 billion out of those $85 billion of foreign exchange reserves, buy gold bullion, and have 100% gold bullion reserve coverage for the Lira, which is an interesting idea.

Or, leaving gold out of it for now, the central bank could support the Lira's value – let's say, raising it back to about 8 per Dollar from 16/Dollar recently – by purchasing Lira in the foreign exchange market.

However, this must be "unsterilized intervention". Otherwise, it won't work. If $1 billion of foreign exchange reserves are used to purchase Lira, then the Lira monetary base must fall by the equivalent of $1 billion (about 16 billion Lira). The Lira purchased by the central bank must disappear.

In practice, it rarely takes a contraction in the monetary base of more than about 20% to support a currency, even during a crisis. That would mean about $7 billion of purchases, out of total foreign reserves of $85 billion. Pocket change.

On top of that, the central bank could pair its foreign exchange sales with sales of domestic assets (such as government bonds). There might be $3.5 billion of foreign exchange sales, combined with $3.5 billion of sales of domestic assets.

Once traders saw that the central bank was not only supporting the currency, but hitting every offer up to a target of 8 Lira/Dollar, and doing so in "unsterilized" fashion with a corresponding direct reduction in the monetary base, traders will have to get on the buy side or risk being annihilated. Remember, the central bank can buy every Lira in existence twice over. It is an absolutely irresistable force – as long as it knows what it is doing.

When they figure out what's going on, traders would quickly buy Lira themselves, getting a free ride from 16/Dollar to 8.5/Dollar. Easy money.

Alongside this, domestic interest rates in Turkey would collapse. Getting paid 10%+ per year, in a reliable currency, is a very, very attractive proposition. Getting paid 10%+ in a currency that is going up a lot is even better. Interest rates would soon fall to low levels.

Once the Lira is stabilized, then the demand for Lira might expand, just as was the case in the 2000s. The central bank, after reducing the monetary base by perhaps 20%, might find that it then has to expand again, just to meet the new demand for more-reliable Lira. It might have to sell Lira in the foreign exchange market, to keep the Lira from rising too much. (This is why foreign exchange reserves expanded so much in the 2000s.)

Alas, all this takes a level of expertise which, as is obvious to all, the central bank of Turkey does not possess. So, let's say a few words about the typical modes of failure, of central banks in these kinds of crisis situations.

The basic problem is "sterilization," where the normal effects of foreign exchange sales (reduction of the monetary base by a corresponding amount) are cancelled out ("sterilized") by purchases of domestic assets, resulting in a monetary base that is unchanged, or even gets larger. This is a model for certain failure. There are two ways in which this seems to come about.

Although direct reductions in the monetary base, to support a currency's value, lead to lower interest rates in a relatively short time, they can also cause very short spikes in overnight interbank lending rates, possibly in excess of 100% per annum for a day or two. This was true, for example, due to the automatic processes of Hong Kong's currency board, in the middle of currency meltdowns throughout Asia in 1998, when overnight lending rates momentarily hit 280%. Thus, a central bank that has some kind of short-term interest rate target would end up expanding the monetary base to reduce these short-term interest rates, effectively "sterilizing" the foreign exchange intervention. In Hong Kong's case, these very short spikes in interest rates had no lasting effect, and the defense of the currency board was entirely successful. Any interest rate targets should be abandoned, to avoid interfering with direct base money adjustment via sales of foreign or domestic assets.

The second cause of "sterilization" seems to be central bank policies of a Monetarist theme, which target a steady growth of base money supply. Foreign exchange sales are "sterilized" by the purchase of domestic assets, to meet Monetarist money growth targets. The monetary base does not contract. A quick reduction of the monetary base, by perhaps 20%, violates all the principles of this Monetarist view, which goes some way to explain why these Monetarist notions are fallacious and destructive. The Monetarists tend to think that, if you reduce the monetary base by 20%, then nominal GDP would also fall by 20%, which could be catastrophic. This is not true: when a currency's value is supported, instead of being allowed to collapse into oblivion, it is very good news for the economy. GDP grows. Focus on the value of the currency, not the quantity. The correct quantity is the one that produces the desired value. Any Monetarist growth targets should be abandoned, to avoid interfering with direct base money adjustment via sales of foreign or domestic assets.

Unfortunately, Turkey has a long history of currency failure, so it would be no surprise if the country were to stack up some new failures today. But, it doesn't have to be that way. In the past, mostly before 1970, the Turkish Lira had long stretches of reliability, and perhaps Turkey will aspire to greatness again.

Email us

Email us