IX Investor Presentation

BullionVault Director Paul Tustain's speech at IX 2006.

Why gold? (and how to buy it)

Good afternoon Ladies and Gentlemen.

Thank you for attending this IX 2006 seminar on Gold.

I am going to be answering two questions you might be asking :-

1. Why would I buy gold ?

2. How would I buy gold ?

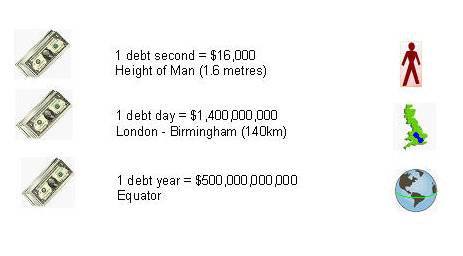

My first slide is a pile of dollar bills. I'm going to use this to illustrate the developing problems in the USA.

I think I've been lucky that in my life America has been the world's superpower. It has been more restrained in the use of its great power than any country which ever found itself at the top of the heap. Being negative about it now feels very ungrateful. So to any Americans in this audience I apologise, but I want to say it as I see it. Everything is being put at risk through reckless American finance.

Every second the US government spends $16,000 more than it raises in taxes - and goes by that amount further into debt. That's a pile of money 1.6 metres high.

Since I have been talking - about 1 minute - this debt has increased by about $1m. By this time tomorrow the debt will have increased by $1,400 million. That would be a pile of money about 140 kilometres high - approximately the distance from London to Birmingham.

By this time next year this debt will have increased by $500,000 million. That is a pile of money 50,000 kilometres high - easily enough to be laid down around the equator.

Here I have only spoken about the budget deficit. The other of the deficit twins is the trade deficit. This is about 50% worse than the budget deficit. It grows as Americans buy consumer goods and export dollars - one of the few great US exports left. America may no longer produce the best cars, or even the best computers, but people widely believe (at least for now) that it produces the best money. That is why it is dollars which are being saved in bulk, all over the world.

The result of exporting dollars is that the world's foreign banks have accumulated reserves of $2 trillion. This is a pile of money about 200,000 kilometres high. It would go round the globe 4 times. Remember that nothing other than the perceived reliability of that money stops it from flooding into the world's financial system.

The US government's aggregate debt is now $8.5 trillion. This is a pile of money 850,000 kilometres high - which would go round the earth 17 times, or take us to the moon and back. Add in commercial US dollar denominated bonds and you get the total of $US denominated bonds - which is $45 trillion, or a pile of money some 4.5 million kilometres high - 90 times round the equator.

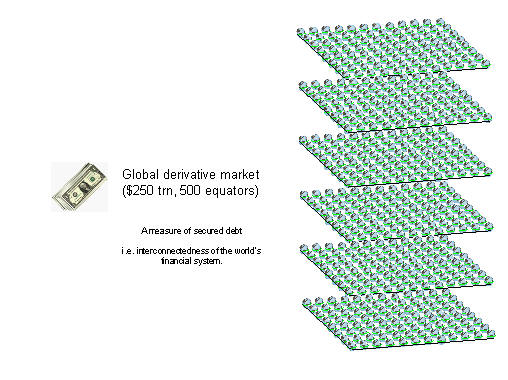

This slide shows the scale of the derivative market. This is estimated at $250 trillion. A pile of money which would go round the earth 500 times.

At this point we need to stop and clarify the difference between bonds and derivatives. The essence of a dollar denominated bond is an unsecured debt. The derivative market is not unsecured in the same way, because where - for example - a future is traded, the open derivative is generally collateralised with margin.

So what this $250 trillion derivative market illustrates is the degree of interconnectedness in modern financial marketplaces. It shows - if you like - how many dominoes have been lined up with the potential to fall if one institution fails. This interconnectedness has grown from about $5 trillion in 1986 to the $250 trillion balance today - which is about 50 times in 20 years.

These are the numbers which describe why people are buying gold. They are frightened of currency devaluation, they are frightened of bond default, and they are frightened of the potential for a severe financial crisis arising from derivatives - what Warren Buffet famously described as 'weapons of financial mass destruction'.

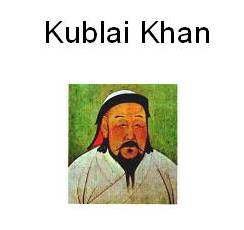

This is a picture of Kublai Khan who lived about 700 years ago. He was the first to issue large quantities of paper money. The Italian explorer Marco Polo visited him in China, and was deeply impressed by Chinese economic management. He wrote how Kublai Khan "had the secret of alchemy in perfection" and how he "causes each year to be made such a vast quantity of money that it must equal in quantity all the treasure of the world".

But Marco Polo had gone back to Italy when the system collapsed. It was left to Alexander Del Mar - an American historian - to describe the breakdown of the system.

"This was the most brilliant period in the history of China. Kublai Khan, entered upon a series of internal improvements and civil reforms, which raised the country he had conquered to the highest rank of civilization, power and progress. Life and property were amply protected; justice was equally dispensed; and the effect of a gradual increase in the currency was to stimulate industry and prevent the monopolization of capital.

Population and trade had greatly increased, but the emissions of paper notes outran both, and the inevitable consequence was depreciation. All the beneficial effects of a currency which is allowed to expand with a growth of population and trade were now turned into those evil effects that flow from a currency emitted in excess of such growth. Excessive and too rapid augmentation of the currency, resulted in the entire subversion of the old order of society. The best families in the empire were ruined"

Since Kublai Khan first showed the way the same trick has been used by dominant economic powers in Spain, France and England. So far each has subsequently failed.

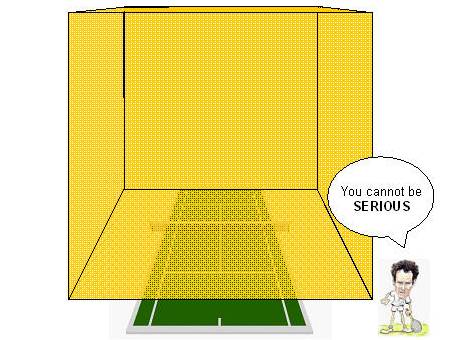

My next slide shows a tennis court.

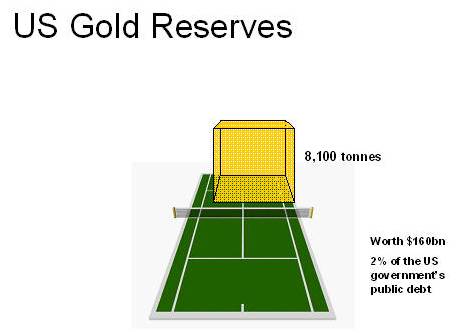

Imagine all the gold in the world, from the Ancients in Egypt and Rome, to the new world gold found by the Spanish Conquistadores, through to the California Gold rush, the Australian, Russian and - biggest of all - South African deposits. Imagine all that gold formed into a single cube. It's edge would be 20 metres. Not quite enough to cover a single tennis court.

The US gold reserve is a 7 metre cube.

It is worth about $160bn, representing 2% of the government's debt.

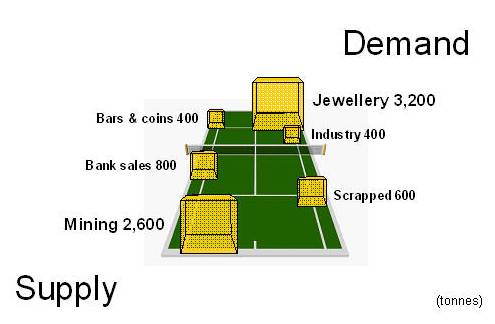

Gold supply is in a competition with demand. Currently the two main players are mined supply at 2600 tonnes and jewellery demand at 3200 tonnes. An important balance has been Bank sales, which provide about 800 tonnes a year from mainly European banks.

Eastern banks, like China, Russia, and also Japan all have large dollar reserves and have recently shown a tendency to be net buyers of gold, rather than sellers which - like our own Gordon Brown - remain mainly European. There is a steady eastwards shift of the world's gold reserves.

The contest between supply and demand is measured by price. This chart shows 30 years of the gold price. It divides into 3 main phases. Firstly from 1970 to 1980 there is a strong rise, during which the investment purchasing power of gold went up 15 fold. This was the second time it did so in the 20th century, because its purchasing power grew 17 times in the deflation of the 1930s.

The second phase was between 1980 and 2000. During this time gold went down from a peak of 850 to a trough of 260. During this period you would have lost about two thirds of your money, while your shares and properties were multiplying. Money invested in shares and houses at this time grew to be 25 times the size of the same money invested in gold.

The third phase is from 2001 onwards. Gold has risen from $270 to $600. This recovery shadows the increasing monetary ill-discipline of the USA, and means that gold has just more than doubled, and in so doing outperformed both shares and houses during the period.

So far in this presentation I have been explaining the reasons for buying gold. Now I want to look at the method.

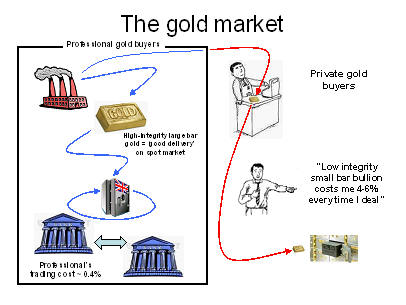

This slide shows the dual nature of the gold market. On the left - inside the 'black box' - is the professional market. On the right is the private market.

Accredited gold refiners produce large bar bullion for the professional market. It is stored continuously in accredited bullion vaults, and traded between member financial institutions. This market trades at what is known as the 'spot' price, which you see published widely in the financial press. But a condition of selling at the 'spot' price is that you must be able to make delivery in a large bar of gold with a complete history of professional vault storage.

If your bar has been in private hands it loses its integrity and will not be automatically accepted as a good delivery to the buyer.

This means private sellers do not benefit from either the highly competitive spot market price, or the depth of the professional market's liquidity. Firstly they usually lack the funds to buy large bars. Secondly they usually don't have access to professional vault storage.

So smaller bars tend to exit the black box of the professionals and be traded via small retail traders. This retail market is much less liquid, and extra costs cause private buyers to pay small bar dealing costs of about 5%. This is more than 10 times the cost of dealing professionally.

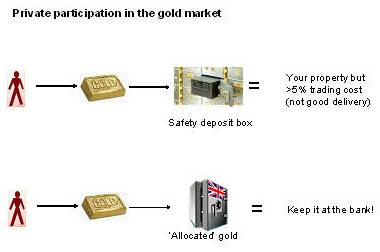

An obvious solution is for the private buyer to hire vault space from a bank - inside the professional market's black box.

But while this is a good solution for the private buyer it is a poor solution for a bank. Banks try to earn returns of 20% per annum on capital. Allocated gold nets the bank about 1% in fees. Banks are far more profitable where they can employ customer assets via deposit accounts.

As a result banks invented 'Unallocated Gold'. This structures the customer's gold as a deposit and demotes the customer from owner to unsecured creditor. Worse still the customer is outside the realm of depositor protection - which applies to currency only. Meanwhile the bank is able to put that gold to its own use - probably as part of its liquidity reserve.

As well as creating Unallocated gold the banks increased the storage charge on Allocated gold to uncompetitive levels. This further encouraged unallocated gold.

This combination virtually eliminated privately owned gold in the custody of banks. Unallocated gold is 99% of the market.

But unallocated gold does not isolate the gold owner from the bank's balance sheet - which is a major objective of many people who buy gold. If more people realised this there would certainly be fewer private buyers prepared to accept unallocated gold.

This next slide explains something of my personal experience.

Back in 2001 I bought some gold from a highly respected Swiss bank. After three interviews and ten weeks I was finally allowed to buy some. The charges were very high, yet even then, after reading the small print, I found out that I only had unallocated gold.

This was the trigger for creating BullionVault.

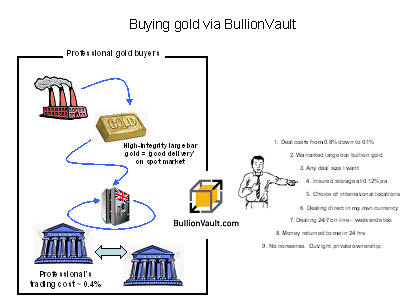

BullionVault acts as a bridge for the individual into the professional gold market. We buy the several large bars at a time which makes gold dealing economic, and we have them sent to Brinks - an accredited bullion vault operator. So the gold retains its professional market integrity and all its resale value. We then let people buy and sell this warranted gold, both to us, and to each other, via our website. This means they can deal in smaller sums but without the loss of spot market integrity and pricing.

Here are the key advantages of buying gold through BullionVault.

1. Deal costs are down from 5% for small bar gold to about 0.8%. On bigger volumes as low as 0.1%.

2. Warranted large bars are high integrity gold. There is less doubt about the quality of the gold you own.

3. You can deal in any size you want.

4. Insurance and storage is 0.12% per annum - less than a tenth of typical Allocated bullion storage at a bank.

5. You get a choice of international storage locations, and can switch between them.

6. You can deal directly in Euros and Sterling - as well as US Dollars

7. Dealing is available all day and every day.

8. Your money can be returned to you in 24 hours.

9. There is no nonsense - you own your gold outright. It is your legal property.

10. We also greatly reduced the time and complexity of dealing. With reasonable efficiency at their banks most of our users are able to buy gold on the day they first make contact with us.

BullionVault has made a big impact on the way people are buying gold. There are already 10,000 users and 2 tonnes of gold in the vaults. It is now easily the biggest provider of privately owned bullion in the UK, and one of the biggest in the world.

Also BullionVault has been extensively reviewed. Here are a couple of comments, and of course you can check out the 'CUSTOMER COMMENTS' section of our website. You'll find them easily from our homepage at www.BullionVault.com.

Finally all of you are welcome at our stand R6, where, under the watchful eye of our Brinks security staff, we invite you to feel for yourself the weight of the London Good Delivery Bar.

Thank you very much for your attention and I look forward to talking to you later.

A bar of professional 'London Good Delivery' gold: Just over 400 Troy Ounces and 99.77% pure. This was on display in a special handling cabinet at IX 2006 - overseen by Brinks security guards. The arch at the front allowed customers to pick up the bar. The value of this bar was about $250,000.

The BullionVault Team at IX 2006. Kris Jenkins, Paul Tustain (Director), Alex Edwards and Catherine Little.

Email us

Email us