Japan Still Leads the Way

Mon, 21-Aug-2023 09:01

First the bubble, then the inevitable...

JAPAN got there first, says Tim Price of Price Value Partners.

A little over 20 years ago, we met a Japanese equity manager who made an astonishing prediction:

"Japan was the dress rehearsal. The rest of the world will be the main event."

That seemed an extraordinary suggestion a little over 20 years ago. Today, not so much.

In the aftermath of the late 1980s real estate and stock market bubble, and its subsequent banking crisis, Japan became a giant laboratory experiment for novel monetary policies.

In 2001 the Bank of Japan tried QE. It was a policy that Richard Koo of the Nomura Research Institute described as the "greatest monetary non-event". It turned out, not for the first time, that academic economists had it all wrong. Borrowers, not lenders, were the fundamental bottleneck in Japan's recession:

"The central bank's implementation of QE at a time of zero interest rates was similar to a shopkeeper who, unable to sell more than 100 apples a day at $1 each, tries stocking the shelves with 1,000 apples, and when that has no effect, adds another 1,000. As long as the price remains the same, there is no reason consumer behaviour should change – sales will remain stuck at about 100 even if the shopkeeper puts 3,000 apples on display. This is essentially the story of QE, which not only failed to bring about economic recovery, but also failed to stop asset prices from falling well into 2003."

It is difficult to appreciate just how much psychological, let alone financial, damage Japan and its investors have endured since the collapse of its late 1980s 'bubble economy'. One estimate has it that, in terms of the subsequent loss of wealth suffered by property and equity prices, the Japanese economy has been hit by the equivalent of not one but two American Great Depressions. Given that measures like GDP growth and unemployment have held up remarkably well over the period in question, and that Japanese society never once threatened to disintegrate into lawlessness or violence, you have to wonder whether the West might aspire to the level of stoicism that the Japanese have displayed.

The central banks of the rest of the developed world have had more success to date in boosting asset prices through their own deployment of QE, but they have had just as little impact on their real economies. What QE has done is made the asset-rich richer, and the poor relatively poorer. (Both trends have been turbocharged by governments' disastrous counter-Covid policies.) But inasmuch as social equality is a stated aim of most governments, QE has been a disaster.

But it has, until recently, done wonders for bond prices. Hypothesis: QE is a lobster-pot for Keynesian central bankers. (And yes, there is no other type.)

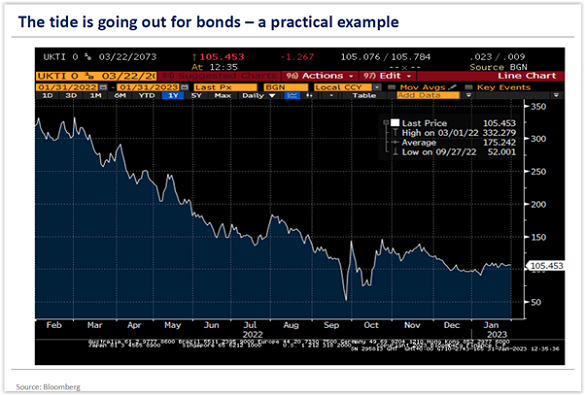

The rot embedded throughout the system became visible last year. As interest rates began to normalise after years near zero, bond prices collapsed. Not just conventional fixed coupon bonds, but index-linked bonds too.

The chart below shows the response of the 2073 inflation-linked UK Gilt, for example, to an environment of higher rates last year. Between January and September 2022, this bond contrived to lose 85% of its value.

So much for the 'risk-free rate'. The Conservative Party responded to this re-arrival of the bond market vigilantes by binning the Liz Truss administration.

Bloomberg's Marcus Ashworth highlights the dangerous game now being played by the Bank of England:

"Since beginning in November, it's been alone among the major central banks in pursuing active selling of its portfolio. It was forced to delay for a month as it cleared up the mess from Liz Truss's gilt crisis, but it's wasted little time since. Funnily enough, none of its central bank peers has rushed to join it as they watch gilt yields zooming above all other major bond markets. It also purchased £20 billion of corporate bonds in 2021 but has exited those holdings at significantly lower prices – and with sterling corporate bond credit spreads wider as a result.

"State assets haven't been disposed like this since then-Chancellor of the Exchequer Gordon Brown liquidated over half of the UK's gold holdings at $275 per troy ounce. The BOE's quarterly analysis shows the QT bill will be far bigger. Not only is the BOE directly competing against the UK Treasury's Debt Management Office in weekly auctions, it's locking in staggering losses for the state – particularly in selling low-coupon long-dated holdings, which have collapsed in value. The gilt market is functioning better than during the 2022 crisis but volatility remains significantly higher than usual."

The debt situation of the US is no stabler. As the website Sovereign Man points out, the US Federal Reserve now has unrealised losses from its bond portfolio of over $910 billion.

"Given that the Fed only has $42 billion in capital, this means that America's central bank has a net financial position of MINUS $868 billion on a mark-to-market basis."

Now Japan and the BoJ seem to have reached their own end-game. Market analyst Joe Consorti:

"The Bank of Japan is launching $2.1 billion in emergency bond-buying only 48 hours after backing away. Inevitable for all central banks that do QE. Your crisis response is now a permanent facility, doomed to maintain stability with perpetual buying. A sovereign debt ouroboros [an ancient symbol of a snake devouring its own tail]."

Investors – and most of their financial advisers – seem to have been mesmerised by four decades of lower interest rates. Newsflash: when interest rates rise from all-time historic lows, as they have these last two years, bad things happen to the prices of financial assets. Notably to bonds and property. In an environment of generalised global overindebtedness, and now uncomfortably high inflation, paper promises start to look disgustingly flimsy.

Ben Hunt of Salient Partners has written convincingly about the power of narratives and their effect on a credulous investing community. The problem now is that narratives that protect the status quo are starting to falter very badly. Brexit was just the first brick to fall off the edifice of Business As Usual. The first Trump government was the second. In a frankly hurried-looking response, the globalists gave us SARS CoV-2 and the Biden crime administration. As Hunt puts it, the Fix is still in, but it's getting harder and harder to maintain:

"...status quo political and economic institutions – particularly Central Banks – have failed to protect incomes and have pushed income and wealth inequality past a political breaking point. They made a big bet: we're going to bail-out / paper-over the banks to prevent massive losses in the financial sector, we're going to inflate the stock market so that the household sector feels wealthier, and we're going to make vast sums of money available for the corporate and government sectors to borrow really cheaply."

Narratives die hard, but when the 'omnipotent central bank' narrative finally and conclusively fails, bond investors will suffer a religious experience as the market rushes to reprice poisonous – but currently still popular – trash.

More central bankers should start listening to Richard Koo:

"Even though QE failed to produce the expected results, the belief that monetary policy is always effective persists among economists in Japan and elsewhere. To these economists, QE did not fail: it simply was not tried hard enough. According to this view, if boosting excess reserves of commercial banks to $25 trillion has no effect, then we should try injecting $50 trillion, or $100 trillion."

We could call such a policy "Krugman's stimulus".

Ben Hunt again:

"Our portfolios should minimize the maximum risk the world actually presents, not maximize the reward our crystal ball models predict. Timing, timing, timing. We need to pay attention to what matters, and right now that's all policy and all Narrative all the time. In a negative [but now rising] rate world, you've got to think in terms of catalysts, not "stocks for the long haul". And one more thing. To paraphrase Groucho Marx in Duck Soup, if a four-year-old can't understand what you're doing in your portfolio, don't do it. For me, that means real assets and real yield, fractional ownership in real companies with real cash flows from real economic activity with real people. You know, what a stock market used to mean before it became a Central Bank casino."

Defensive value stocks; uncorrelated funds; real assets, and notably the precious metals. That's how we're positioned for the fire sale of everything else. Did we not say? The main event is now shaping up to be a disaster movie. 'Great Reset' would be putting it mildly.

Email us

Email us